July 2026 Issue #11 | |||

Record Highs in Stocks and Headwinds on the Horizon | |||

THE BIG 3__ About FaceInflation and Growth are poised to flip. __ New Fed New RulesIs this the last dot plot? __ Crypto TearsSo much for fiat currencies failing. |  | ||

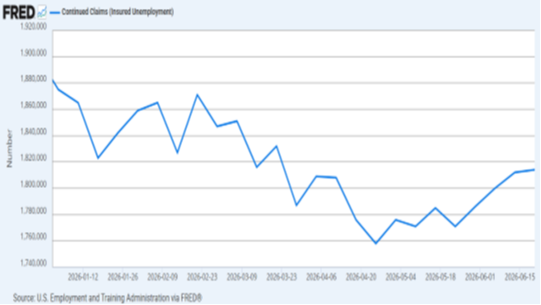

About FaceElevated inflation does not mean Accelerating inflation. Our base case was for inflation to remain elevated into Q4 of 2026. This still remains true, but in rate-of-change terms, we now expect inflation to look less bad (as in not accelerating). Over the shortest of terms, we expect both growth and inflation to decelerate, with inflation decelerating at an accelerating pace until Q4. Based on current data and our modeling, we expect inflation to print at or near 3.9% for June and decelerate further to 3.5% in July. Theoretically, growth should slow as well; however, our best predictor of GDP is jobs data while we wait for quarterly estimates to be released. Given that fact, new jobs declined precipitously at the end of Q2, while ongoing unemployment claims ticked up in the last report. This would indicate a potential for a growth slowdown. As such, we have moved from a seemingly confirmed Stagflationary regime in Q2 to a shallow Disinflationary regime in Q3. | |||

| Crypto TearsThe entirety of the crypto universe has faced a meltdown in 2026. What we are seeing:

| ||

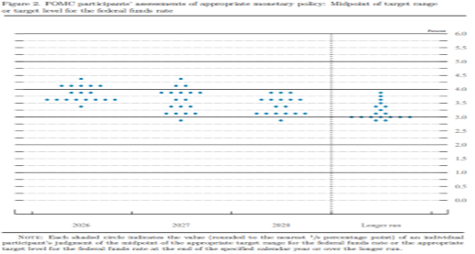

New Fed Chair = New RulesThe Kevin Warsh era is officially underway. The first question that comes to mind is, “What’s the over/under in months that Trump will try to fire Warsh?” Considering he was nominated with the explicit mandate of cutting rates, Warsh openly opined on the potential need for rate hikes. More important than the rate hike narrative is the fact that the Fed is no longer going to openly provide forward guidance. It is our view that the reasoning behind this is two-fold. There is the real-world application of being truly data-dependent. That would be a nice change. On the flip side, the Fed’s predictive modeling has been comically insufficient over the last few years. We think Warsh wants the Fed to cease being the punchline for so many economic cartoonists. This could very well repair the Fed’s reputation if he handles things correctly. At least that is the best-case scenario. | |||

| The Bottom LineTrying to time a market that effectively changes growth and inflation regimes on a monthly basis is not possible at scale. If anything, less forecasting from the Fed will create additional volatility as policy changes are no longer telegraphed. While this theoretically provides the Fed with more flexibility to manage faster economic cycles, it will take most investors a while to adapt. This is where quality economic research and forward-looking asset allocation has a generational opportunity to shine. | ||